Geopolitical Shock: How the United States Aggressive Foreign Policy Shift is Affecting the American and Global Economy

Source: Harold Mendoza

On January 3rd, the United States military captured Venezuelan President Nicolás Maduro and his wife, Cilia Flores, in a special operation, “Operation Absolute Resolve”. Elite U.S. forces conducted the raid in Caracas overnight, which included strikes on military infrastructure in Caracas. Following the capture, they were flown to New York to face charges related to drug trafficking and narco-terrorism. The capture followed months of increased U.S. pressure and targeted action against the Venezuelan government.

On February 28th, after ongoing failed negotiations and movements of ships and troops into the Middle East. A joint coalition of Israel and the U.S launched major military strikes against Iran, killing the supreme leader, Ayatollah Ali Khamenei. While Venezuela was swift, the consequences of striking Iran have led to a full-scale conflict in the region. President Donald J. Trump declared that the objective of the operation was to destroy Iran's missile and military capabilities, prevent Iran from obtaining nuclear weapons, and ultimately to achieve regime change.

The United States, in less than two months, has displaced two leaders of enemy countries closely allied with China and Russia. The events of early 2026 represent the most aggressive pivot in U.S. foreign policy since the early 2000s, with the transition from economic sanctions and proxy diplomacy to direct intervention. Trump saw sanctions as weak and ineffective and proved to the world that no “enemy” leader is safe and the American military can apprehend “you” at any time. By using raids or direct strikes, he is attempting to cut the lengthy time it would take to force regime change in these nations, where leaders have held executive power for decades.

Initial shift in oil prices after Maduro's capture

Following the U.S. intervention and change in leadership in Venezuela in early 2026, global oil prices generally fell, with Brent crude dropping to around $60 and WTI Crude to $57 a barrel. Brent Crude oil prices fell by approximately 2% to 2.5%, and WTI Crude fell 1.2% to 1.7%, in the immediate aftermath, driven by market expectations of a long-term supply glut. A supply glut occurs when supply significantly outpaces demand, leading to falling prices and built-up inventories. As the U.S. move signaled the eventual return of Venezuela's massive crude reserves to the global market, the massive influx of supply is greater than the current demand, and prices will eventually fall, but not have a significant impact in the short-term. Traders anticipated this when Venezuelan barrels returned to the market, and analysts suggest that while Venezuela holds 17% of proven global reserves, it will take years and billions in investment to restore production to the 3 million barrels per day of the 1990s. Meanwhile, under Maduro, during the economic crisis in the 2010s, it was below 1 million, and at its worst, around 500,000 BPD. Oil production over the past month has increased by 200,000 BPD, reaching 1,000,000 BPD.

China loses approximately 55% of the Venezuelan oil exports it had been receiving, forcing a costly pivot to Russian and Iranian alternatives. Beyond the supply disruption, China has roughly $10–12 billion in Venezuelan debt and $2.1 billion in oil sector investments that are now at serious risk under a U.S.-aligned government in Caracas. Perhaps more damaging strategically, Venezuela was a key node in China's sanctions-evasion oil network, providing deeply discounted barrels outside Western financial systems. China is partially cushioned by record stockpiles and its diverse supplier base, so this is not an immediate crisis, but it represents a meaningful strategic and financial setback.

The U.S. is well-positioned to benefit, as Gulf Coast refineries are purpose-built for heavy crude exactly like Venezuela's, creating a natural and highly profitable match. The U.S. now controls Venezuelan oil revenues, with proceeds flowing into U.S.-managed accounts, giving Washington financial leverage. New OFAC licenses have opened the door for American companies to re-enter Venezuelan oil fields at scale. The key obstacle is economics: projections break even around $80 per barrel, well above the current $57–60 price range, meaning large-scale investment is unlikely to materialize until prices rise or production costs fall significantly.

Cuba faces the most severe and immediate consequences of almost any nation in the world. Both Venezuela and Cuba have been regional enemies of the United States and align themselves with China and Russia. Cuba was receiving roughly 50% of its oil from Venezuela under a barter arrangement, and that supply is now effectively cut off. The country was already suffering 10–20-hour daily blackouts even before the full cutoff, and conditions have worsened sharply since. Cuba has no foreign currency reserves to purchase oil on open markets, and U.S. pressure has successfully deterred Mexico and other potential suppliers from stepping in by using tariffs on anyone who sells oil to Cuba. The U.S. has issued a narrow license permitting Venezuelan oil sales to Cuba's private sector only. The overall strategy appears designed to use energy strangulation as a pathway toward regime collapse.

Overall, China loses a key energy supplier and has to turn to alternative sources; meanwhile, the United States seems to have a long-term plan for Venezuelan oil and has not had a significant impact yet. However, with Cuba, the United States is trying to end another regional regime while they have the chance, but in the short term, it is affecting inflation domestically. As Mexico and other regional players navigate the Cuba Tariffs, the cost of imported goods from these nations is rising. This adds to the inflation currently hitting the U.S. manufacturing and grocery sectors.

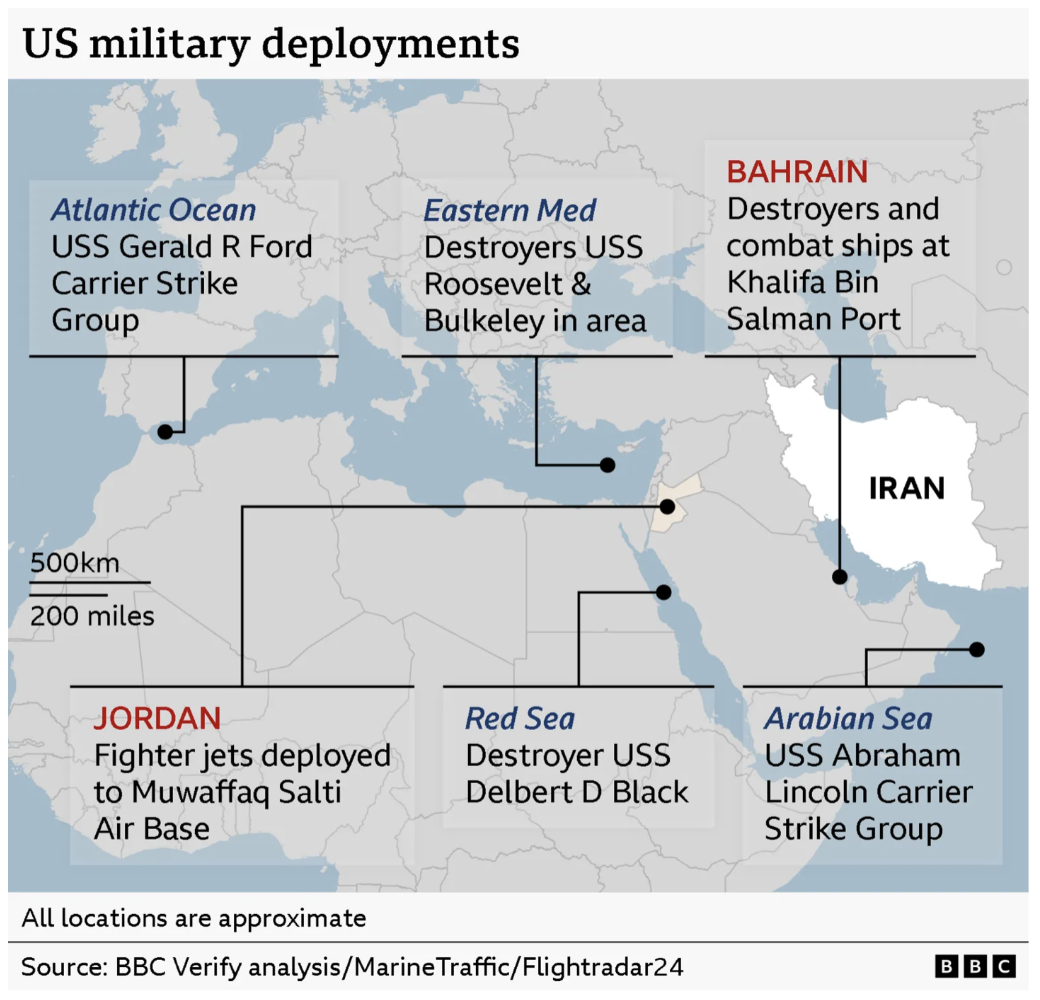

U.S. and Israeli Strikes Against Iran Spiked Oil Prices

Across the world, the Middle East has been a hotbed of proxy wars in recent decades, while also being a major producer of global oil. With reasoning shifting as the war progresses, the striking of Iran appears to have less to do with the acquisition of resources, but more with regime change to deter a nuclear program in Iran. That isn’t to say that oil was not affected—it definitely was.

Source: BBC

One of the first major global economic shocks from the strikes was Iran's closure of the Strait of Hormuz. The Strait carries approximately 20% of global petroleum consumption, roughly 20 million barrels per day, flowing from major Gulf producers like Saudi Arabia, Iraq, the UAE, Kuwait, and Qatar to the rest of the world. Iran's Islamic Revolutionary Guard Corps (IRGC) declared the strait closed and threatened that any vessel attempting to pass would be set ablaze, effectively bringing shipping through the waterway to a near halt, with hundreds of ships sitting idle. This is categorically different from the Venezuela situation; rather than a supply glut and a gradual price decline, the Iran conflict has created a sudden, acute supply shock.

The conflict caused Brent crude to surge 10% to 13% to around $80 to $82 per barrel by March 2, 2026, and, at its peak, prices rose from around $70 to over $110 per barrel within days as the disruption in the Strait of Hormuz set in. This effectively reverses and then dramatically overshoots the slight price declines that followed the situation in Venezuela. As of early March, Brent crude was trading at $83.75 per barrel, with prices remaining volatile.

Airlines were among the hardest hit, with United, American, and Alaska Air each falling more than 4% on high-volume trading days as projections of jet fuel costs climbed sharply. The consumer discretionary sector declined 5.3% overall, with retailers, apparel, and luxury brands retreating as households reallocated spending away from discretionary purchases toward energy and essentials. Consumer goods giants like Procter & Gamble and Unilever faced a compounding pressure with rising logistical costs on one side and falling consumer demand on the other.

Global indices reflected the divergent exposure of different economies. Japan's Nikkei 225 fell 5.2%, reflecting Japan's near-total dependence on energy imports, while the Euro Stoxx 50 declined by approximately 1% and China's Shanghai Composite fell by 0.7%. The S&P 500 saw more moderate single-session declines of 0.7% at the index level, but with significant dispersion beneath the surface.

The Energy Tax on American Consumers

Every $10 increase in oil prices reduces U.S. consumer spending by an estimated 0.2–0.3%. With oil rising from approximately $70 to over $100 at the peak, the aggregate demand drain on the American consumer is significant, functioning as an informal tax that bypasses Congress and disproportionately strikes lower- and middle-income households. National gasoline prices climbed above $4 per gallon (the highest since late 2023), triggering a financial reset for American consumers. Every sustained $ 10-per-barrel increase in oil costs the average U.S. household approximately $450 per year. With oil at $100+, the annualized household burden runs well into the thousands of dollars, competing directly with mortgage payments, rent, and grocery bills. The key recession thresholds that economists are monitoring: oil at $125 per barrel, gasoline at $4.25 per gallon, and inflation reaching 4%. As of March 2026, two of those three thresholds are within striking distance.

The recession risk for both the U.S. and European economies has risen materially since the strikes in Iran. In the U.S., the combination of a deteriorating labor market, persistently above-target inflation, consumers being squeezed by energy costs, and a Fed unable to cut rates creates a challenging macro environment. Europe, which lacks the energy production buffer the U.S. enjoys as a net exporter, is considered by many analysts to be at genuine risk of a technical recession if the conflict persists.

Developing economies face the sharpest risks. Oil-importing nations in sub-Saharan Africa and South Asia, particularly those reliant on Gulf states for fuel supply, face import price shocks. The compounding effects of higher energy and fertilizer prices on food security in these regions represent a serious humanitarian and political risk, with the potential to destabilize fragile states.

The Winners

Not all economies lose from the shock. Large net energy exporters outside the Gulf, whose production capacity is unaffected by the conflict, most notably Norway, Russia, and Canada, stand to gain significantly from elevated prices. For Russia in particular, which has been operating under Western energy sanctions, higher global oil prices effectively increase the purchasing power of its exports even at discounted prices.